Belgium’s frozen billions, still unspent four years later

31 March 2026 /

Artemiz Van den Broucke 6 min

December 12th, 2025. A crowd stands before the European Council calling for Russian frozen assets to be used to pay for Ukraine’s reconstruction and for an end to this war. Their multi-lingual chants aimed to rekindle pressure on the EU to put their money where their mouth is. Months later, has this determination thawed? Has the plan to utilise these funds melted away? As February marked the beginning of the fifth year of the Russia-Ukraine war, the debate over immobilised Russian assets appears perhaps as frozen as the assets themselves. Rather than asking what Europe should do, another question emerges: what is Europe both willing and able to do to help Ukraine finance this fight?

A recap

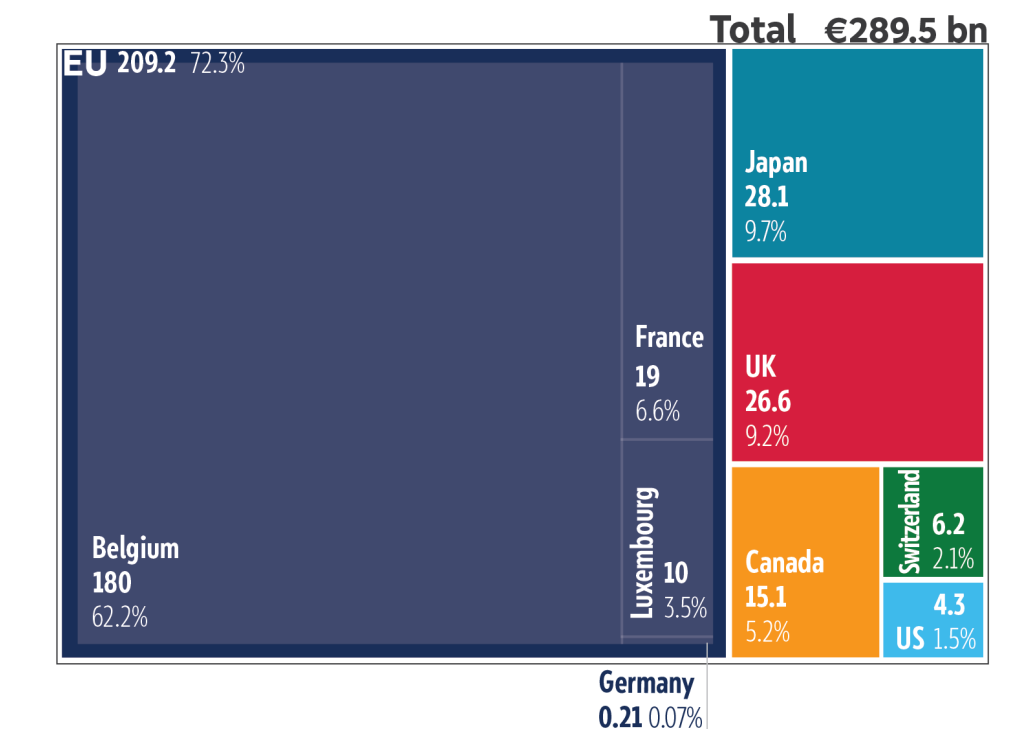

In February 2022, within days of the full-scale invasion, Western governments moved decisively to immobilise the Russian Central Bank’s (CBR) assets under their jurisdiction, marking a significant escalation from individual restrictions like travel bans. Immobilisation or freezing meant that without transferring legal ownership, all transactions related to the assets were now blocked, while interest would still be generated. The total worth of these Russian sovereign assets has an estimated value of €300 billion worldwide [figure 2]. Crucially, a huge portion of these assets, €180 billion according to Bruegel, are managed by Euroclear, a Brussels-based securities depositary that is partially owned by the Belgian federal government, which holds a 12% stake.

Immobilised Russian assets: Main EU and non-EU jurisdictions, 2025 (€ billion)

Source: EPRS, data from PISM, Swiss Federal Government. For Luxembourg, where estimations vary from’several billion euros to around €20 billion’, the authors opted for a conservative figure (€10 billion).

But what is Euroclear?

Hardly an asinine question, before the invasion, Euroclear faced little scrutiny within public discourse. However, with assets in its custody exceeding €43 trillion, more than double the GDP of the EU, this institution has become the face of one of the most consequential financial and legal stand-offs of our era. Before 2022, Euroclear, which describes itself as serving “the public good by ensuring the efficiency of markets and actively enabling the reduction of risk”, routinely served Russian entities. When sanctions froze those assets, the interest and dividends generated were moved to a blocked account. These proceeds were reinvested into the European fund for Ukraine and the cash generated from the matured bonds invested at the European Central Bank via overnight deposits as well as the Belgian central bank. However, as the war escalated, some leaders hoped for more: to unfreeze the funds and channel them directly into Ukraine’s defence and future reconstruction.

Does Belgium bear the burden?

Euroclear’s Director General, Valérie Urbain, vociferously condemned the proposal to reappropriate these immobilised assets into a multi-billion injection into Ukraine’s defence fund. Speaking with Le Monde, she was unequivocal: the plan could trigger Russian legal action and she would not rule out suing the EU. Reuters reported that such moves would drastically affect Euroclear’s “long-term issuer default ratings of ‘AA’, short-term IDRs of ‘F1+’ viability ratings of ‘aa’ and debt ratings”, no doubt also influential in Urbain’s stance.

The high concentration of the €210 billion frozen reserves under EU jurisdiction in Belgium turned up the heat considerably for Belgium’s Prime Minister, Bart de Wever, who shared Urbain’s opposition and similarly cited legal and financial risks. Indeed, his concerns that Belgium would be taking on an incommensurate burden via such focus on Euroclear were lent credence, given that several other member states (Germany, France, Sweden, Cyprus and Luxembourg) and non-EU nations (UK, US, Switzerland and Japan) hold Russian assets according to the European Parliament’s (EP) Research Service. The concern found an unlikely interlocutor in President Zelensky himself, with The Brussels Times reporting the two met privately during the December 18-19 Summit. The Ukrainian leader warned that failure to unfreeze the funds would precipitously reduce drone production and crucial military capacity which Ukraine cannot afford to lose.

The €90 billion compromise

So how to proceed? Billed as a make-or-break moment, the December 2025 Summit aimed to produce an answer. After it was made clear that Belgium’s assent was central to the outcome, the alternative joint-loan plan, needing unanimous approbation from member states (MS), looked similarly glacial in prospect. However, after Hungary, Slovakia and Czechia agreed to refrain from vetoing in exchange for exemptions, a result was reached. The EU has committed to raising €90 billion in the form of bonds floated on capital markets. Euronews reports that Ukraine can hope to receive the first tranche of this loan in early April, followed by a steady flow of disbursements.

The latest

For now, Belgium’s frozen billions remain unspent. The very same assets whose immobilisation represented a historically bold sanction may ultimately be little more than a form of collateral, their interest used to service the borrowing costs of this €90 billion loan that, in an attempt to assuage Ukraine’s mounting debt, Europe will absorb. As well as not paying interest, Ukraine will not be required to begin repayment until Russia ceases its aggression and pays reparations. Given that the Kremlin has categorically refused to compensate Ukraine, that moment remains a distant and uncertain prospect.

The latest news on the frozen billions came in the form of Euroclear’s annual results for 2025, published last month, which showed interest accrued on these assets totalled €5 billion – a 26% fall from the previous year. Of this, €3.3 billion will be allocated to support Europe’s Ukrainian fund. To illustrate the gap between revenues generated and funds made available, the first instalment generated in this way and made available to the European Commission on 23 July 2024 totalled a comparatively modest €1.5 billion. If this trend of percentage decrease continues, the interest-loan combination approach will only prove inadequate and detrimental, as the EP projects Ukraine risks running out of money in early 2026 without international intervention.

Footing the bill?

So, left with a non-recourse loan with debt rolled over into an indefinite future, how might citizens react? Germany, France, Italy, Spain and Poland will carry the highest costs. However, as this is all occurring exclusively at the EU level, it will not count towards any MS domestic debt. Cold comfort, but worth noting. Moreover, beneath the institutional mechanics lies another fundamental question. One that leaders and policymakers might elide but citizens might increasingly be asking: why does Europe need to pay at all? Ukraine’s defence has been framed as inseparable from EU security but critics argue that the fiscal burden falls on taxpayers not institutions. Are commitments to Ukraine sustainable amidst rising domestic tensions, from energy transitions to ageing populations? The autumn 2024 Eurobarometre showed 87% of Europeans agree with continued humanitarian support to those affected by the war in comparison with 58% supporting financing military equipment to Ukraine. How should policymakers interpret and respond to this percentage drop when drafting long-term strategies? One underlying reality remains: four years on from Russia’s invasion, rather than having spent these frozen Russian billions, Europe is still the one spending.

Frozen decisions, heat in the Middle East

Today, the frenetic churn of Trump-era geopolitics has further complicated the picture. Euronews reported Russia pocketed €7.7 billion from two weeks of war in Iran between 1 and 15 March. So as Washington’s attention is diverted to the Middle East and Vladimir Putin remains, for now, the primary geopolitical beneficiary of volatility and hesitation, the debate appears frozen. An EU-level indemnity mechanism could, for example, provide key reassurance, transforming a national liability into a collective European verdict. Europe has consistently framed this war as existential. It is time to act accordingly.